Advertisement

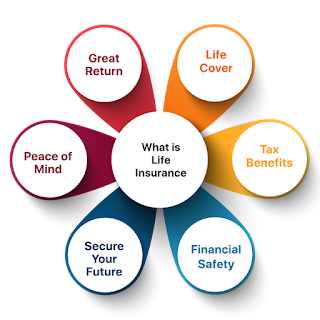

What is life insurance?

A life insurance policy generally pays a lump sum amount of money when you pass away. The money is given to the people nominated as beneficiaries on your policy. Your beneficiaries can choose to use the money to cover mortgage and credit card payments, child care, school fees, and other living expenses.

|

| Life Insurance |

Life insurance is designed to provide a financial safety net if you were to:pass away or become diagnosed with a terminal illness

become seriously injured

become permanently disabled.

During difficult times, this type of insurance can offer a lump sum of money that could help your family afford their debts (e.g. their home loan) and living expenses (e.g. school fees) – even if you weren’t able to support them.

So, how much life insurance do you need? It’s simple enough; you need to be insured for the amount required to maintain the lifestyle your family has grown used to.

For some, this means getting insured for the difference between two variables. The first variable is what your family receives in:superannuation and insurance payouts

dividends from shares

savings.

The second is any debts or living expenses they might have to pay.

You can estimate the level of cover you should consider with our life insurance calculator. Otherwise, if you want to learn more, here’s life insurance explained.

What is term life insurance?

Term life insurance could help financially support your beneficiaries (e.g. your family) if you were to pass away or receive a terminal illness diagnosis. This policy is a common type of life insurance offered by Australian insurers.How does life insurance work?

When you take out life insurance, you sign a contract with an insurer and agree to pay the policy premiums regularly. In exchange, your insurer pays a lump sum of money to your listed beneficiaries (e.g. spouse, children) if you pass away, become seriously ill or injured or become permanently disabled in accordance with the policy’s Product Disclosure Statement (PDS). Life insurance must be purchased before any of these instances occur.Life insurance either covers you for an agreed-upon term (e.g. for the next 10 or 20 years) or, for some insurers, until you reach a certain age. This type of cover is also usually risk-rated, which means your premiums will be calculated based on how likely you are to make a claim; as such, life insurance may cost more for high-risk individuals.

Also, you may need to sit through waiting periods before you can claim on your life insurance. Waiting periods will be clearly outlined in your Product Disclosure Statement (PDS).

How much does life insurance cost in Australia?

How much life insurance costs in Australia, on average, will vary between each person. The cost of life insurance is based on your age, gender, health, smoking status, occupation, lifestyle and other risk factors. How much your life insurance costs will also depend on the type of policy, what your policy covers, and whether you choose stepped or level premiums.For example, you can typically lock in a cheaper rate with a level premium structure. However, level premiums typically still change in line with inflation (CPI) and generally change if:your lifestyle or risk factors become different;

you alter your policy; or

you reach a certain age (usually 65).

On the other hand, a stepped premium usually starts out cheaper than a level premium but gets more expensive as you get older. You may wish to consider whether you’d prefer cheaper premiums now (stepped) or more affordable premiums over time.

To determine how much life insurance may cost you, you can compare life insurance quotes using our online comparison service.

Do I need life insurance?

This is a decision you’ll need to make based on how you believe your family will cope financially if you weren’t able to support them.Specifically, you may need to consider how your family could fare if they needed to pay off debts or cope with regular expenses without your income.

Life insurance also allows you to leave an inheritance to help your children get ahead if you’re no longer around.

You’ll need to take out a policy before a covered event occurs, like a severe injury, for example. So, if you become seriously injured and then take out a life insurance policy, you wouldn’t be able to claim this injury on your cover.

It’s also worth noting that many superannuation funds include a level of life insurance. Unsure if you already have life insurance through your superannuation? Call up your super fund to check, as that cover may be insufficient for your needs.

Advertisement

![What is Insurance | Insurance Meaning and Types | Why insurance is important [2021]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEg4o720bpBs1yJH_HoO0NQSuc1WBVkaG1ttedsfJoDGJSm6DbDzsn4aWR25b6KthW3OcO-1JC3NTSbcmV6Aa6VBQrbIrJbIfZmR7nxqa4DsjLXv6eYUxd0CxWd2kPDjd6YeRA9JLbzlvSE/w320-h320-p-k-no-nu/What+is+Insurance++Insurance+Meaning+and+Types++Why+insurance+is+important+%255B2021%255D.jpg)

![[ Hindi] Car Loan - Compare Best Interest Rate Online](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEj37scwMuKhNz81RBSSdEqwVHA1X2X3jGSVRhTTuVaXqhulqVwM5K22Yl9MCTT5mOUdirlBAMXim-idCbQ9gA_F8yIKJpuP40EPX2_c4EyTpy4tCOhoJxsYZbQe1BtXuwiaB-DLWVQSsBIH/w320-h320-p-k-no-nu/car+images.png)

{kind=link}